Our Top 5 Recommendation

A debit card is different from a credit card because it immediately takes the usage fee from your bank account. This makes it popular for people who worry about spending more than their credit limit.

On the other hand, debit cards have a disadvantage when it comes to redeeming points compared to credit cards. However, some debit cards now have rates higher than 1.0%. As cashless payment methods become more common, the number of debit cards being used is increasing.

In this article, we will not only give recommendations for desirable debit cards but also offer a variety of useful information. This will cover topics such as the various types of debit cards, ways to compare them, strategies for making the best choice, and exploring their pros and cons.

2 Types of Debit Cards

There are two categories of debit cards:

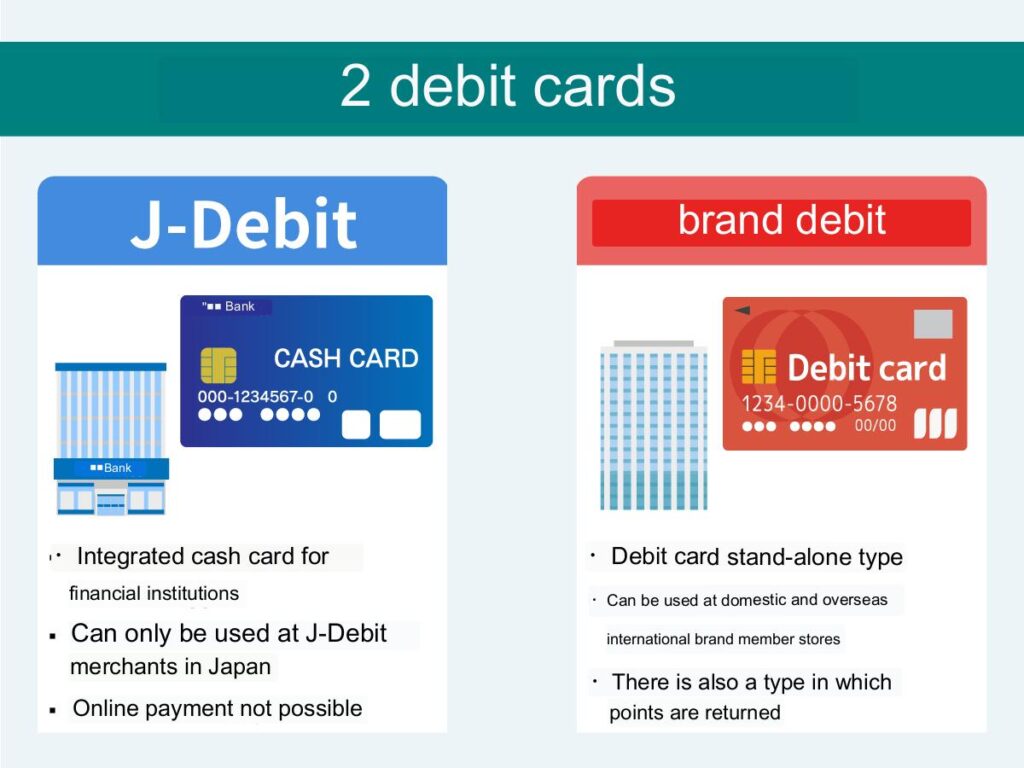

- J-Debit

- Brand debit

The term “J-Debit” is used to describe a debit card that is linked to a cash card issued by financial institutions like banks.

In contrast, “brand debit” refers to a type of debit card that carries the name of an international brand, such as Visa or Mastercard®.

What is a debit card?

A debit card is a type of card that allows for electronic payments and is connected to a bank account.

When a debit card is used, the funds are immediately deducted from the linked bank account.

One key feature of a debit card is that it provides a convenient payment method for individuals who have bank accounts.

Unlike credit cards, which allow payment to be delayed, debit cards do not require repayment at a later date. This makes it a straightforward and immediate payment option.

1. J-Debit Card

“J-Debit” is a specific type of debit card that allows you to use your cash card as a debit card. However, it’s important to know that J-Debit can only be used at stores in Japan that are part of the J-Debit network.

Compared to more recently introduced brand debit cards, there are fewer places where J-Debit can be accepted for payment.

- Supermarkets and convenience stores: 28 nationwide

- Drugstores: 319 nationwide

- Restaurants and food: 920 nationwide

*Reference: Stores that accept J-Debit (Japan Electronic Payment Promotion Organization)

*As of August 2022

Moreover, it’s important to note that J-Debit cannot be used for online payments. Therefore, when it comes to making purchases online, you will need to use alternative payment methods.

2. Brand Debit Card

“Brand debit” refers to debit cards that have well-known international brands like Visa. These brand debit cards can be used at a wide range of stores worldwide that are affiliated with the global brand.

Additionally, some brand debit cards offer point rewards that can be redeemed, similar to how credit cards work. However, it’s essential to know that not all brand debit cards with the same international brand offer the same point redemption rates.

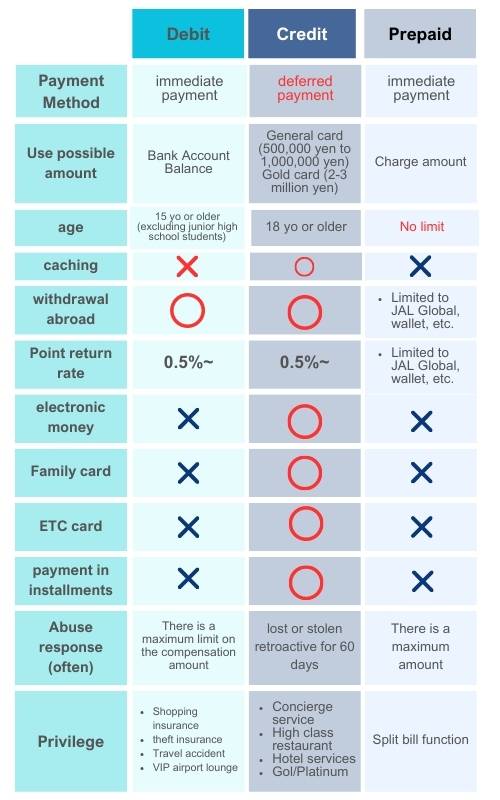

Next, I will explain the differences between the three types of cards used for cashless payments: debit cards, credit cards, and prepaid cards.

Differences between debit cards, credit cards, and prepaid cards

Three types of cards can be used for cashless payments: debit cards, credit cards, and prepaid cards.

Refer to the comparison chart to understand the differences between them.

One important aspect of debit cards is that they are directly linked to the balance in your bank account. This is similar to prepaid cards, as both allow you to make immediate payments without worrying about future bills. The key difference, however, is that with a debit card, you can use it anytime as long as you have enough money in your bank account, without any additional charges.

When it comes to credit cards, the gap between them and debit cards is narrowing as credit cards offer more comprehensive points redemption and benefits. However, debit cards still have a smaller network of merchants compared to credit cards, making them slightly less versatile in terms of usability.

So far, we have discussed the differences between debit cards, credit cards, and prepaid cards. If, after considering these comparisons, you believe that getting a credit card is more suitable for your needs, please refer to the following article for recommendations on popular credit cards.

6 Debit Card Benefits

Debit cards have the following advantages:

- Easy to manage money without overspending

- Relatively easy for anyone to make

- Earn points and cashback

- No need to line up at the ATM

- Withdraw local currency from overseas ATMs

- with fraud protection

Let’s look at each benefit in turn.

Easy to manage money without overspending

One significant advantage of using a debit card is that the money is immediately taken out of your bank account when you make a purchase. The amount you can spend with the debit card is directly linked to the balance in your bank account, making it easy to understand and manage your finances effectively.

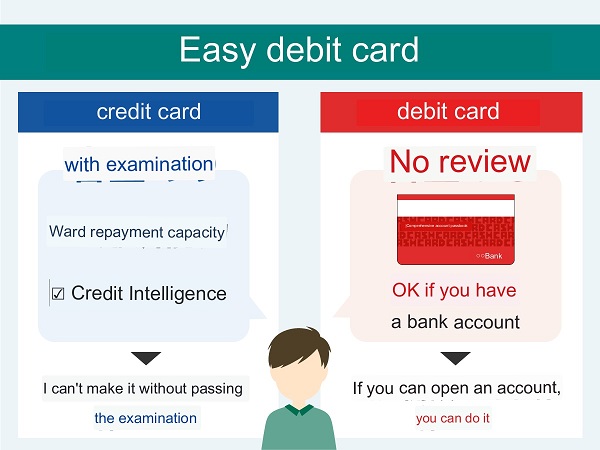

Relatively easy for anyone to make

One advantage of debit cards is that they are accessible to a wide range of people when it comes to opening a bank account.

Unlike credit cards, which involve deferred payments and require a thorough assessment of your ability to repay, individuals with consolidated debts or a history of bankruptcy often struggle to qualify for a credit card. This limitation prevents them from participating in online shopping and creates various inconveniences in today’s modern world.

On the other hand, debit cards are relatively easier to obtain for anyone with a bank account. While they may lack certain features like low point redemption rates and additional services, they provide a similar payment experience to credit cards, allowing individuals to lead a lifestyle relying on card transactions.

Earn points and cashbacks

Some debit cards provide rewards in the form of points or cash back, similar to credit cards, where a percentage of the amount spent is given back to the cardholder.

These types of debit cards are especially suitable for individuals who prefer not to have a credit card and want to avoid making payments at a later date.

By using such a debit card, individuals can enjoy the convenience of cashless transactions while receiving benefits similar to those offered by credit cards.

However, it’s important to be aware that the redemption rates for points and cash back may vary even within the same card. So, it’s advisable to be cautious and carefully consider the return rate if you want to maximize your rewards.

No need to line up at the ATM

Unlike a traditional cash card, which requires you to withdraw money in advance from an ATM, a debit card enables you to make payments without the need for physical cash. This means you can avoid the hassle of waiting in line at an ATM and have the convenience of making purchases directly with your card.

Withdraw local currency from overseas ATMs

Debit cards can be used to withdraw local currency from ATMs in foreign countries. Each transaction at these ATMs usually includes an ATM usage fee of 110 yen (including tax), along with an overseas administration fee ranging from approximately 2% to 3% of the transaction amount.

However, it’s important to note that certain ATMs may charge an additional fee set by the local financial institution.

While credit cards offer similar functionality, it’s crucial to remember that any transactions made using them are considered deferred payments. This means you have to repay the amount later, similar to cash advances, and you may also have to pay interest charges on top of it.

On the other hand, with a debit card, you can instantly withdraw as much local currency as you need without worrying about interest, although there is a fee involved.

with fraud protection

Debit cards provide protection against fraudulent use, which is a major benefit. However, it’s important to understand that there are limits to the maximum amount and specific conditions for compensation.

This means that the refund you receive in case of fraudulent activity may not be as large as you expected initially.

Now, let’s consider the downsides of debit cards, taking into account the information we’ve discussed so far.

5 Debit Card Disadvantages

- Cannot be used if the balance is insufficient

- The rate of return is set too low

- Payment in installments, revolving payments, and cash advances cannot be used

- Basically, ETC cards cannot be issued.

- Not available at some stores

I will go into detail about each item.

Cannot be used if the balance is insufficient

Using a debit card depends on having enough money in your bank account. If there is no balance available, the card cannot be used.

Moreover, if unexpected deductions like automatic utility bill payments cause a shortage of funds, it can be inconvenient because you won’t be able to make necessary payments.

One drawback of relying on a debit card connected to a bank account is the requirement to consistently keep an eye on your balance to prevent any potential inconveniences.

The rate of return is set too low

Debit cards have a disadvantage when it comes to their point redemption rate, which is usually lower compared to credit cards. While it’s true that credit cards have also seen a decrease in their point return rates recently, there is still a difference between debit cards and credit cards in terms of the rate offered. Credit cards generally provide a more favorable point return rate.

Therefore, when compared to credit cards, the relatively lower point redemption rate remains a drawback of using debit cards, as having a higher rate of point return is generally preferred.

Payment in installments, revolving payments, and cash advances cannot be used

Using installment payments, revolving payments, or cash advances with credit cards leads to the accumulation of interest fees. However, these features can be helpful when you need immediate funds or when your income is temporarily reduced. Debit cards, in contrast, do not offer postpay services, which means users miss out on the benefits of deferred payment.

Installment payments, revolving payments, and cash advances are important advantages of credit cards, as they allow individuals to delay payment until a later date.

Basically, ETC cards cannot be issued.

Debit cards and prepaid cards, except for the Hokkoku Visa Classic Debit card, cannot be used to obtain ETC (Electronic Toll Collection) cards. Typically, a credit card is required to get an ETC card. However, for individuals who are unable to obtain a credit card due to their credit history, there is an alternative option called the “ETC Personal Card,” which doesn’t have credit functionality. It might be worth considering this alternative.

Furthermore, there is an article available that provides recommended methods for people who cannot obtain an ETC card with a debit card. If you’re interested, I suggest referring to that article for more information and guidance.

Not available at some stores

The usage of debit cards is increasing, but it’s still unfortunate that many stores don’t accept them. However, if you have a debit card with the well-known Visa or Mastercard® logo, you’ll find that it’s generally accepted by a wider range of merchants.

In contrast, J-Debit cards issued by banks have limited acceptance at stores. Therefore, it’s important to check whether they can be used before making a transaction.

Now, let’s examine the five disadvantages of debit cards.

How to Compare and How to Choose the Right Debit Card

How to compare debit cards

Consider the following four points when choosing a debit card.

- Annual fee

- Point redemption rate/cashback redemption rate

- International brands

- Bank services that issue debit cards (ATM fees, transfer fees)

Most regular debit cards do not have an annual fee, but it’s important to be aware that gold and platinum class debit cards, similar to credit cards, often come with an annual fee.

When choosing a debit card, it’s crucial to check the point redemption rate and cashback redemption rate to make sure they match your preferences.

Debit cards with internationally recognized brand logos are accepted at many stores, which makes them worth considering.

Additionally, it’s important to evaluate the overall usability of the bank that issues the debit card, not just the card itself. High ATM fees and transfer fees can lead to unnecessary expenses, so it’s necessary to take these factors into account.

How to choose

Considering the pros and cons discussed earlier, there are important factors to think about when getting a debit card. Here are some considerations:

- Choose a good bank debit card

- If you want to use it at many stores, “Brand debit” with international brands

- If you often use overseas, “Visa” is convenient for international brands

- Consider the balance between usage patterns, annual membership fees, and point/cash return rates

- If you want to combine payments such as utility bills, check the status of the support

- For those who do not want to carry a card, consider the convenience of using a smartphone

I will explain each in detail.

Choose a good bank debit card

When selecting the best debit card from a good bank, it’s important to consider your options carefully. The debit card is directly linked to your bank account, allowing for immediate payments without carrying balances into the following month or beyond. Choosing the right debit card is similar to choosing the bank itself.

For example, if you maintain a fixed balance in your account, such as a salary transfer account, it’s advisable to choose a bank that offers a debit card with suitable features. Opting for a bank that doesn’t charge account management fees for debit card usage can add to the convenience. Aeon Bank is an example where using their own ATMs may not incur any fees.

For those interested in opening a new bank account specifically for a debit card, net banking is recommended. While there may be transfer fees involved, the high point return rate makes it a favorable option worth considering.

If you want to use it at many stores, “Brand debit” with international brands

If you want to be able to use your debit card at many different stores, it’s worth considering getting a “brand debit” card that carries international brand logos. This greatly increases the number of stores where your card will be accepted, making it very convenient for online shopping or regular purchases.

If you often use overseas, “Visa” is convenient for international brands

If you travel abroad often, especially outside of Japan, choosing a Visa debit card offers great convenience. Visa is widely accepted worldwide, making it a perfect choice for business trips, travel, or studying abroad. With a Visa debit card, you can easily make transactions and payments in various countries.

If you plan to use your debit card primarily in Europe, it is recommended to choose a Mastercard as it provides wide coverage in the region. While other card brands can also work well, it can be advantageous to prioritize Visa or Mastercard based on your specific usage patterns. Both Visa and Mastercard are widely accepted in Europe, making it convenient for various transactions and purchases during your time there.

Consider the balance between usage patterns, annual membership fees, and point/cash return rates

It’s important to find a balance between your usage patterns, annual membership fees, and point/cash return rates when choosing a debit card. If you use your card infrequently or moderately, it’s recommended to select a card with no annual fee and a high return rate to maximize the benefits you can get.

On the other hand, if you use your card frequently, a card with an annual membership fee might be more suitable as it often comes with additional services. When making a decision, evaluate your usage frequency and consider the return rates offered by different cards.

If you want to combine payments such as utility bills, check the status of support

If you plan to use your debit card for combining payments like utility bills, it’s important to check if the chosen debit card supports such transactions. Unlike credit cards, debit cards are increasingly being accepted for paying utility bills, including pensions and mobile phone bills.

However, the compatibility for these payments can vary among different debit cards. It’s advisable to visit the official website or contact the support center of the card issuer to confirm if your specific payment needs can be met. Consolidating payments into a debit card can simplify the management of your household finances.

For those who do not want to carry a card, consider the convenience of using a smartphone

If you prefer not to carry physical cards, using your smartphone for electronic payments can be very convenient. Many debit and credit cards now support electronic payment options, allowing you to make payments without needing the physical card.

However, it’s important to know that not all electronic payment methods are universally supported. For example, Apple Pay has fewer compatible cards compared to Google Pay. Additionally, smartphone payment options like Pay Pay and d payment offer alternative solutions.

To find the most convenient option for you, evaluate which debit card suits your usage needs best. Here are five recommended debit cards to consider.

Compare 2 Recommended Japan Debit Cards

| card | GMO Aozora Net Bank “Mastercard Platinum Debit Card” | GMO Aozora Net Bank Debit |

| Annual fee | 3,300 yen (tax included) | free |

| return rate | 1.20% | 0.6-1.2% |

| international brands | ||

| Issuing speed | Shortest same day | about 2 weeks |

| feature | High return & benefits higher than annual membership fee | Cash card and debit card integrated |

2 Recommended Debit Cards

- GMO Aozora Net Bank “Mastercard Platinum Debit Card”

- GMO Aozora Net Bank Debit

1. GMO Aozora Net Bank "Mastercard Platinum Debit Card" with high return rate

GMO Aozora Net Bank "Mastercard Platinum Debit Card"

| Annual fee | First year: 3,300 yen (tax included) 2nd year onwards: 3,300 yen (tax included) |

| Point redemption rate | 1.20% |

| International brands | |

| Electronic money | – |

| Issuing speed | about 2 weeks |

| Credit limit | Up to 10 million yen |

| ETC annual fee | |

| additional card | |

Mileage redemption rate (maximum) | |

| travel insurance | |

| point name |

attention point

- 1.2% cash return!

- ATM fees and transfer fees are free 20 times a month!

- The usage limit is 10 million yen per day, so it can be used for large purchases!

- 5,000,000 Yen/Year Unauthorized Use Compensation Included!

- Smartphone payment supports PayPay and d payment

The GMO Aozora Net Bank Mastercard Platinum Debit Card offers cashback rewards instead of points. It also serves as a cash card, eliminating the need to carry multiple cards with you.

Advantages

- A single card can be used to pay utility bills and taxes

- It supports Visa touch payment and is highly convenient

- The usage limit is 10 million yen per day, so it can be used for large purchases!

By using a regular debit card, you can often avoid ATM withdrawal fees and fees for transferring money to other banks, usually for a limited number of times, such as two or three times. However, the GMO Aozora Net Bank Mastercard Platinum Debit Card goes a step further and provides the advantage of 20 free transactions per month, which offers even greater convenience.

Moreover, this card is compatible with smartphone payment methods like Pay Pay and d payment, allowing you to make payments through your smartphone.

Additionally, it offers various protective measures to ensure security and peace of mind.

Disadvantages

- If you don't raise your customer rank, you may get less benefit

- Annual membership fee

While the GMO Aozora Net Bank Mastercard Platinum Debit Card offers valuable benefits, it’s important to note that these benefits come with certain conditions. If you don’t use the card frequently, the cashback rate will remain at 0.6%, and you will still have to pay the ATM usage fee at least twice.

It’s essential to be cautious and consider if these conditions align with your usage patterns. Additionally, there is an annual membership fee of 3,300 yen, so the benefits may not be as advantageous for users who don’t use the card frequently.

GMO Aozora Net Bank “Mastercard Platinum Debit Card” is recommended for these people!

- People with high payment frequency and high usage amount

- Who wants a Mastercard debit card

The GMO Aozora Net Bank Mastercard Platinum Card is a great choice for people who use it often and have significant expenses.

Although there is an annual fee, if you take full advantage of the card’s benefits, the potential rewards can outweigh the cost. Additionally, the card provides strong security measures, making it a valuable option for those who heavily rely on debit cards.

2. Up to 1.2% cashback "GMO Aozora Net Bank Debit"

GMO Aozora Net Bank Debit

| Annual fee | First year: Free Second year and beyond: Free |

|---|---|

| Point redemption rate | 0.6% to 1.2% |

| international brands |

|

| Electronic money | |

| Issuing speed | about 2 weeks |

attention point

- Cash back up to 1.2% of the usage amount!

- No issue fee, no annual fee!

- Supports Visa touch payment

This debit card has distinct features compared to the GMO Aozora Net Bank Mastercard Platinum Debit Card mentioned earlier. While there are notable advantages when the card brand is Visa, there are also other benefits worth considering.

Advantages

- A single card can be used to pay utility bills and taxes

- It supports Visa touch payment and is highly convenient

- You can save money on shopping because it supports PayPay and d payment

With this debit card, you can conveniently cover all your expenses using just one card. It is highly recommended for individuals who prefer managing their income and expenditures in one place.

Not only is the card itself convenient, but you can also earn various points by making it compatible with payment platforms like PayPay and d payment. This allows you to enjoy additional benefits while using the card for your everyday transactions.

Disadvantages

- If you don't raise your customer rank, you may get less benefit

- Annual membership fee

While this debit card supports PayPay and d payment, it’s important to note that it does not support smartphone payments. Additionally, the maximum point redemption rate is 1.2%, which is considered average. For individuals who value higher point redemption rates, it may feel slightly unsatisfactory.

However, please understand that this debit card is designed for people who prioritize usability and convenience.

GMO Aozora Net Bank Debit is recommended for these people!

- People who emphasize usability rather than return rate

- People looking for a debit card that can be used overseas

Since this debit card carries the Visa brand, it can be used in a wide range of locations overseas. However, it’s important to note that the fee for using it abroad is relatively high at 3.08%.

Despite this, the card is highly recommended for individuals who prefer using one card for all their payments. The point redemption rate is considered average and not low, making it a suitable choice for those who have some concerns about the redemption rate.

How to Get a Debit Card

There are three main ways to get a debit card.

- Apply at store

- Apply by mail

- Apply online

I will explain in detail how to make each one.

Apply at store

If you don’t have a bank account, it may be necessary to apply for one in person. Here’s what you need to do:

Visit a designated store: Go to a store that offers banking services and follow the procedures for opening a bank account.

Provide identification documents: During the account opening process, you will need to provide identification documents and a personal seal (stamp). Typically, two types of identity verification documents are required, such as a document with your photograph (e.g., My Number card, driver’s license, passport) and a health insurance card or resident’s card.

Consult the official website: Make sure to check the official website of the specific debit card you want to apply for to gather all the necessary information.

Application submission and delivery: Once you submit your application, the debit card will be sent to you via simple registered mail within approximately 1-2 weeks.

If you don’t have an existing bank account with the institution where you want to obtain the debit card, it’s recommended to apply in person. This way, you can avoid the need to apply separately for both opening a bank account and getting a debit card.

Apply by mail

To apply for the debit card by mail, follow these steps:

- Acquire an application form from the store or online platform.

- Complete the application form by providing the required information.

- Make copies of the mentioned identity verification documents.

- Enclose the copies of the documents along with the completed application form.

- Send the application by mail.

From this point on, the process will be similar to applying at a physical store.

This method is recommended for individuals who are unable to visit the store due to time constraints or lack of internet access.

Apply online

At present, the majority of debit card applications are conducted online. Here’s the simplified process:

Apply Online:

- Complete the application form online.

- Take a photo of your identity verification document and submit it electronically.

- Provide facial patterns for identity confirmation if required.

Convenience and Availability:

- Online applications are available 24/7, allowing you to apply at any time.

Processing Speed:

- After submitting your application, the processing speed for card issuance is similar to other methods.

Recommended for Certain Situations:

- Online applications are recommended for those who can’t visit a physical counter or prefer to apply without time constraints.

Now that you know how to obtain a debit card, let’s move on to understanding how to effectively use the card.

How to use debit card

Here are three ways to use your debit card.

- When used in a physical store

- When using an online shop

- When using overseas

Let’s take a quick look at how each is used.

When using debit card in a physical store

When shopping at physical stores, it’s important to check if your debit card can be used there. Specifically, for J-Debit cards, look for the J-Debit mark displayed on the cash register.

If you don’t see the mark, it’s recommended to ask the store staff directly to confirm if your card is accepted before proceeding with your shopping or dining experience.

When it’s time to make the payment, follow the procedure by either passing your card through a dedicated machine or using touch payment if available. If the store clerk asks how many payments you want to make, simply respond with “One-time payment.”

When using debit card in an online shop

When shopping online, choose the credit card payment option and provide the required information, including the card number, expiration date, and security code.

Once you’ve entered these details, the payment will be deducted from your bank account through immediate settlement, and the payment process will be completed.

When using a debit card overseas

When you want to withdraw local currency from ATMs abroad, it’s important to verify if your debit card is accepted at the ATM beforehand. Once confirmed, you can proceed with the withdrawal process. Your bank account will be debited immediately, and you will receive the local currency based on the exchange rate of the day.

I have already provided information on how to use a debit card.

Lastly, we have prepared a list of frequently asked questions about debit cards for your reference.

Frequently Asked Questions

Debit cards can be made by high school students over the age of 15 .

Since the balance of the bank account is the upper limit of the amount of use, there is no question about income.

Even if you don’t have a part-time job, you can make it without any problems.

If you have the debit card in your possession, immediately contact the phone number on the back of the card to cancel the transaction.

If you lose your card, check the emergency contact information on the debit card’s official website on the Internet and take procedures to suspend the use of the card.

Q3:Can I change the debit card account?

Summary

A debit card is a convenient card that allows you to withdraw cash and make cashless payments immediately. It is directly connected to your bank account, so you don’t have to worry about paying back money in the future as you spend within your available balance. It promotes responsible financial management.

However, not all stores accept debit cards, so it’s important to check before using one. Unlike credit cards, debit cards don’t offer installment plans or revolving payments. It’s crucial to plan your expenses carefully to avoid depleting your funds too quickly.

When used wisely, debit cards are a practical and convenient payment option. Take the time to choose the right debit card for your needs and remember to use it responsibly.

- Author: Shunya